Introduction to Blockchain Technology and Its Applications

- Understanding the Basics of Blockchain Technology

- Exploring the History of Blockchain and Its Evolution

- The Key Components of Blockchain Technology

- Real-World Applications of Blockchain in Various Industries

- Challenges and Opportunities in Implementing Blockchain Solutions

- The Future of Blockchain Technology: Trends and Innovations

Understanding the Basics of Blockchain Technology

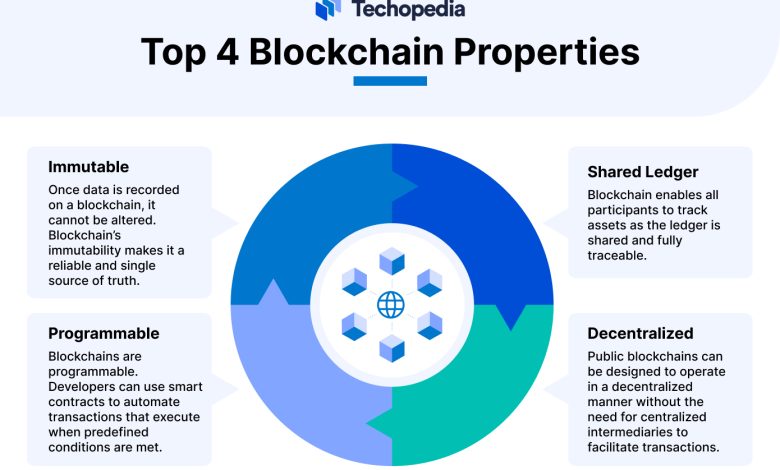

Blockchain technology is a decentralized, distributed ledger system that records transactions across multiple computers in a secure and transparent manner. The basic concept of blockchain involves a chain of blocks, where each block contains a list of transactions. These blocks are linked together using cryptographic hashes, creating a secure and tamper-proof record of transactions.

One of the key features of blockchain technology is its transparency. All transactions recorded on the blockchain are visible to all participants in the network, providing a high level of accountability. This transparency helps to prevent fraud and ensures the integrity of the data stored on the blockchain.

Another important aspect of blockchain technology is its security. The use of cryptographic algorithms and decentralized consensus mechanisms make it extremely difficult for malicious actors to alter the data stored on the blockchain. This makes blockchain technology ideal for applications where data security is paramount.

Blockchain technology has a wide range of applications across various industries, including finance, supply chain management, healthcare, and more. In the finance sector, blockchain technology is being used to streamline cross-border payments, reduce transaction costs, and improve transparency. In supply chain management, blockchain technology is being used to track the movement of goods from the manufacturer to the end consumer, ensuring authenticity and preventing counterfeiting.

Overall, blockchain technology has the potential to revolutionize the way we store and transfer data. Its decentralized and secure nature makes it an ideal solution for a wide range of applications, offering increased transparency, security, and efficiency. As the technology continues to evolve, we can expect to see even more innovative use cases emerge in the future.

Exploring the History of Blockchain and Its Evolution

Blockchain technology has a rich history that dates back to the early 1990s. It was originally conceptualized by Stuart Haber and W. Scott Stornetta as a way to timestamp digital documents to prevent tampering. However, it wasn’t until 2008 when an individual or group of individuals using the pseudonym Satoshi Nakamoto introduced blockchain as the underlying technology behind the digital currency Bitcoin. This marked the beginning of blockchain’s evolution from a niche concept to a revolutionary technology with far-reaching applications beyond cryptocurrency.

Over the years, blockchain has undergone significant advancements and adaptations to meet the growing demands of various industries. One of the key milestones in blockchain’s evolution was the development of Ethereum in 2015 by Vitalik Buterin. Ethereum introduced the concept of smart contracts, which are self-executing contracts with the terms of the agreement directly written into code. This innovation opened up a whole new world of possibilities for blockchain applications, enabling decentralized applications (dApps) to be built on top of the Ethereum blockchain.

As blockchain technology continued to mature, new consensus mechanisms such as Proof of Stake (PoS) and Delegated Proof of Stake (DPoS) were introduced to address scalability and energy efficiency issues associated with traditional Proof of Work (PoW) consensus. These new mechanisms allowed for faster transaction processing and reduced energy consumption, making blockchain more sustainable and environmentally friendly.

The evolution of blockchain technology has also seen the rise of enterprise blockchain solutions tailored to meet the specific needs of businesses. Companies across various industries are exploring the use of blockchain for supply chain management, identity verification, and secure data sharing. The potential cost savings, increased transparency, and enhanced security offered by blockchain technology have made it an attractive option for organizations looking to streamline their operations and improve trust among stakeholders.

In conclusion, the history of blockchain is a testament to its transformative potential and the continuous innovation driving its evolution. From its humble beginnings as a timestamping tool to its current status as a foundational technology for the digital age, blockchain has come a long way in a relatively short period. As blockchain technology continues to evolve, we can expect to see even more groundbreaking applications and use cases emerge, further solidifying its position as a game-changer in the world of technology.

The Key Components of Blockchain Technology

Blockchain technology consists of several key components that work together to create a secure and transparent system for recording transactions. These components include:

– **Decentralized Network**: Blockchain operates on a decentralized network of computers, known as nodes, that work together to validate and record transactions. This decentralized nature ensures that there is no single point of failure, making the system more secure and resilient.

– **Blocks**: Transactions are grouped together into blocks, which are then added to the blockchain in a linear, chronological order. Each block contains a list of transactions, a timestamp, and a reference to the previous block, creating a chain of blocks.

– **Cryptography**: Cryptography plays a crucial role in blockchain technology by ensuring the security and integrity of transactions. Each transaction is encrypted using complex mathematical algorithms, making it virtually impossible for hackers to alter the data.

– **Consensus Mechanism**: In order to add a new block to the blockchain, the network must reach a consensus on the validity of the transactions. This is typically done through a consensus mechanism, such as Proof of Work or Proof of Stake, which requires nodes to solve complex mathematical puzzles to validate transactions.

– **Smart Contracts**: Smart contracts are self-executing contracts with the terms of the agreement between buyer and seller directly written into lines of code. These contracts automatically execute when certain conditions are met, eliminating the need for intermediaries and streamlining the transaction process.

By understanding these key components of blockchain technology, we can begin to see the potential applications and benefits of this revolutionary technology in various industries.

Real-World Applications of Blockchain in Various Industries

Blockchain technology has found applications in various industries, revolutionizing the way businesses operate and interact with customers. Some of the real-world applications of blockchain include:

- Finance: In the financial sector, blockchain is used for secure and transparent transactions, reducing the need for intermediaries and speeding up processes. It also enables the creation of smart contracts, automating agreements between parties.

- Supply Chain Management: Blockchain technology is utilized to track and authenticate products throughout the supply chain, ensuring transparency and reducing the risk of counterfeit goods entering the market.

- Healthcare: In the healthcare industry, blockchain is used to securely store and share patient data, ensuring privacy and accuracy of medical records. It also helps in tracking the authenticity of drugs and medical devices.

- Real Estate: Blockchain technology is employed in real estate for property transactions, enabling faster and more secure deals. It also facilitates the tokenization of assets, allowing for fractional ownership of properties.

- Government: Governments are exploring the use of blockchain for voting systems, identity verification, and secure document storage. This technology can help in reducing fraud and increasing transparency in public services.

These are just a few examples of how blockchain technology is being implemented across different industries, offering benefits such as increased security, transparency, and efficiency. As the technology continues to evolve, we can expect to see even more innovative applications in the future.

Challenges and Opportunities in Implementing Blockchain Solutions

Implementing blockchain solutions presents both challenges and opportunities for businesses across various industries. One of the main challenges is the complexity of integrating blockchain technology into existing systems. This process requires a deep understanding of how blockchain works and how it can be tailored to meet specific business needs. Additionally, ensuring the security and privacy of data on the blockchain is crucial, as any vulnerabilities could lead to potential breaches and compromises.

On the other hand, there are numerous opportunities that come with implementing blockchain solutions. One of the most significant advantages is the transparency and immutability of the blockchain, which can help increase trust among stakeholders. Blockchain also enables faster and more secure transactions, reducing the need for intermediaries and streamlining processes. Moreover, blockchain technology has the potential to revolutionize supply chain management, healthcare, finance, and many other industries by providing a decentralized and tamper-proof ledger for transactions.

Overall, while there are challenges to overcome in implementing blockchain solutions, the opportunities for businesses to innovate and improve efficiency are vast. By carefully navigating the complexities of blockchain integration and leveraging its unique features, organizations can position themselves at the forefront of technological advancement and gain a competitive edge in the market.

The Future of Blockchain Technology: Trends and Innovations

The future of blockchain technology is filled with exciting trends and innovations that are shaping the way we interact with data and conduct transactions. One of the key trends in blockchain technology is the rise of decentralized finance (DeFi), which aims to create a more inclusive financial system by eliminating the need for traditional intermediaries. This trend has the potential to revolutionize the way we access financial services, making them more accessible and affordable for everyone.

Another important trend in blockchain technology is the development of non-fungible tokens (NFTs), which are unique digital assets that represent ownership of a specific item or piece of content. NFTs have gained popularity in recent years, with artists, musicians, and other creators using them to monetize their work and engage with fans in new ways. The use cases for NFTs are constantly expanding, with potential applications in gaming, collectibles, and even real estate.

In addition to these trends, there are also several innovations on the horizon that could further enhance the capabilities of blockchain technology. One such innovation is the development of scalable blockchain solutions that can process transactions more quickly and efficiently, making them suitable for a wider range of applications. Another innovation is the integration of blockchain technology with other emerging technologies, such as artificial intelligence and the Internet of Things, to create more powerful and versatile systems.

Overall, the future of blockchain technology is bright, with new trends and innovations constantly pushing the boundaries of what is possible. As the technology continues to evolve, we can expect to see even more exciting developments that will transform the way we live, work, and interact with the world around us.